- Blockchain is a technology that relies on cryptography and decentralized networks to create secure and tamper-proof records, thereby eliminating the need for intermediaries and establishing trust.

- Other major companies are currently utilizing blockchain for payments, supply chains, healthcare and digital identity.

- Our point is that blockchain doesn’t require any technical knowledge, as the internet does today in everyday life.

Whether you’ve crossed borders with money, purchased a home, or even wondered where your food comes from, you’ve relied on systems that haven’t changed much over centuries. So, what is blockchain? It is a revolutionary technology designed to create secure, transparent, and decentralized systems that could disrupt the way we exchange value and trust information.

Let me explain what blockchain is in simple terms. It’s no longer just a technology for the crypto community or tech enthusiasts. Blockchain is quietly transforming how the world operates — from finance and healthcare to supply chains and digital identity. Understanding it is no longer optional; it’s becoming essential.

What is blockchain in a nutshell?

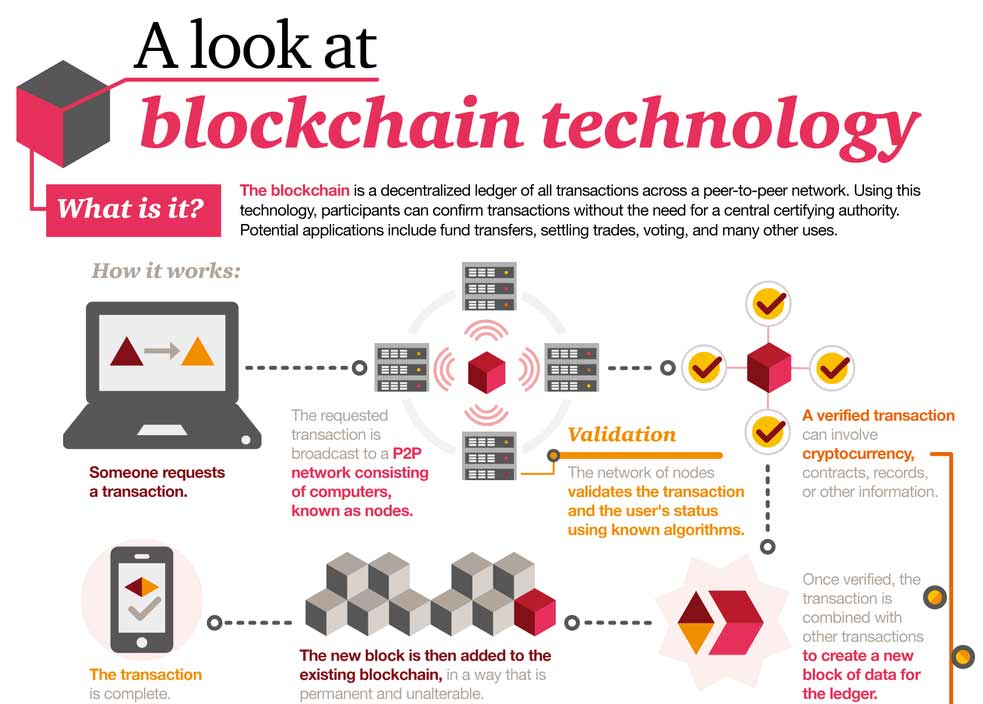

Let go of any preconceived notions you may have about Bitcoin for now. Blockchain is just a digital “notebook” that is duplicated on thousands of computers all around the world. Everyone else sees it, verifies it and permanently records it when someone writes something in this notebook. The second it’s in there, nobody can delete or alter it. Not you, not me, nor any bank, nor any government.

It’s as easy as envisioning a Google Doc that thousands of people can view at the same time, yet no one can edit or delete the previous entries. Each new entry gets a time stamp, is added to the preceding entry, and remains permanently fixed. That series of secured entrances? That’s the “blockchain.” Gary Fox’s depiction of the process includes broadcasting a transaction to a peer-to-peer network of nodes, which validates them and shares the consensus with others, and then permanently appending them to the chain.

The magic lies in three main points: decentralized (no one owns it), immutable (data is not liable to manipulation) and transparent (anyone can see the data). The blockchain industry will grow to $20 billion, up from the $400 million in 2017, as described by 101 Blockchains.

The working of blockchain: Transactions are transmitted to a network of nodes, these nodes verify the transaction, and the transaction is then permanently recorded on the blockchain.

What is the point of it? The Real-World Impact

Okay, so it’s a fancy notebook. But what is the relationship between that and you? The conventional method of establishing trust is costly, slow, and flawed. To understand what is blockchain, think of it as a digital system that replaces traditional trust mechanisms with a secure and transparent way of verifying information.

When you go to purchase a house, you need a couple of things checked: You have to involve lawyers, title companies, and banks to make sure that the person selling the house is the rightful owner and that you can afford it. If you send money abroad, it may pass through 3–5 banks over 3–5 business days, with each bank taking a cut. Similarly, when you purchase organic coffee, you have to trust the label that claims it is genuinely organic.

Blockchain eliminates the need for many of these intermediaries. It establishes trust without relying on a single authority or organization. It allows people and businesses to verify transactions directly, creating a shift from a trust-based world to a trustless one by enabling the secure transfer of trust.

Here’s where Blockchain is having an immediate impact.

This is no more theoretical now. As of 2026, blockchain is already providing solutions to everyday problems:

1. Cross-Border Payments

International transfers are usually made in days and incur 2-3% fee. Blockchains, such as Ripple, process transactions in less than three seconds and at a much lower cost. Major financial firms are no longer experimenting with blockchain, but deploying it, as Investra’s 2026 business guide shows, J.P. Morgan’s Onyx platform already has billions of dollars worth of transactions running on the rails of blockchain.

2. Supply Chain Transparency

Recall the “lettuce” scare? Blockchain can make it possible to trace a contaminated product back to its exact origin lot in seconds, rather than days. Major grocery retailers are now demanding blockchain-based provenance from suppliers, according to Classic Informatics. Unlike the traditional paper-based tracking, you can literally scan a QR code on your avocado and see the full journey from farm to shelf!

3. Healthcare Data

At present, your medical records are spread across dozens of non-communicating medical systems. While blockchain won’t store patient health information directly on the blockchain, it’s used to demonstrate who can access what, and it makes it secure and patient-controlled. This way, you keep your data private, and still have the interoperability that healthcare is longing for.

4. Smart Contracts

No paper, no claims department and no waiting — imagine a flight insurance policy that does that automatically when flights are more than 2 hours late. This is a smart contract! Investra does it automatically when conditions are fulfilled, eliminating human error and delay in contractual arrangements, as explained by Investra.

5. Digital Identity

Paper credential verification is slow and cumbersome. With Blockchain, people can have a digital wallet that stores verifiable digital credentials such as degrees, licenses, IDs and more. Classic Informatics points out that credentials can be issued by a university, you can carry them and any employer can instantly verify them without reaching out to the university, saving weeks of verification time.

From finance to healthcare, blockchain is reshaping industries with its decentralized, transparent systems.

The Bigger Picture: Why This Matters for the Future

Let’s dispense with the skeptics: blockchain is not just about speeding up existing processes. It’s about reconstructing the concept of truth and trust in a digital age. Understanding what is blockchain reveals why this technology is becoming a foundation for secure, transparent, and reliable digital systems.

Researchers, including those at the National Institutes of Health, have highlighted blockchain’s ability to remove single points of failure and strengthen cybersecurity. Distributed ledgers are being adopted by companies as a risk-management tool to reduce vulnerabilities as cyberattacks become more frequent and costly. One of the key advantages of blockchain is its cryptographic security, which helps ensure that stored data remains tamper-resistant — a critical feature in today’s increasingly digital world.

Blockchain is expected to merge with AI and IoT to form automated and verifiable systems, according to the World Economic Forum and others. By 2030, according to Plasma.org’s analysis, blockchain will be the foundation of autonomous economic agents, a concept that is similar to that of the smart contracts, but where, instead of the human user, the smart contract will be triggered automatically by an IoT sensor, or by your smart fridge, ordering milk when it is running low, with payment and delivery verified on the blockchain without human intervention.

Investra reports that Gartner’s Hype Cycle has enterprise blockchain well on its way from the “Trough of Disillusionment” to the “Slope of Enlightenment” phase, indicating progress from speculation to progressive application across a limited number of valuable lines of business. The change marks a shift from “will it work” to “where does it work best”.

Common questions and answers (FAQs)

Q1: What is the difference between blockchain and bitcoin?

What is blockchain is a common question for beginners, especially when comparing it with Bitcoin. Bitcoin is only one use case of a blockchain. Imagine blockchain is the internet and Bitcoin is one website on the internet. There are many other applications that do not involve cryptocurrency, such as supply chain traceability, digital voting, healthcare records, and identity verification, which can be powered by blockchain technology. In this post, Classic Informatics explores the impact of blockchain adoption beyond cryptocurrencies and how it is transforming industries worldwide.

Q2: Yes, blockchain is secure. Can it be hacked?

Yes, blockchain is designed to be highly secure.

The decentralized and cryptographic structure of blockchain makes it difficult to manipulate. The distributed ledger design ensures there is no single point of failure, making large-scale data tampering extremely challenging. NIH cybersecurity research highlights how blockchain can improve security by reducing centralized vulnerabilities. However, blockchain-based applications, such as exchanges or poorly coded smart contracts, can still have weaknesses. The security of the technology is rarely the issue — proper implementation is the key factor.

Q3: What is the difference between blockchain and a normal database?

A traditional database is controlled by a single entity, such as a bank or company, and authorized users can edit or delete information. Blockchain works differently by distributing data across thousands of computers, where recorded information becomes extremely difficult to alter or remove.

Each block contains a unique hash that connects it to the previous block. If someone changes one block, the entire chain is affected and the modification becomes immediately visible. This is one of the reasons what is blockchain technology has become an important topic for understanding the future of secure digital records.

Q4: Will blockchain replace banks and governments?

Not likely. Blockchain is not designed to replace institutions; it is a technology that helps improve existing systems. Instead of removing banks and governments, it is more likely that these organizations will adopt blockchain to provide faster, cheaper, and more transparent services. Major financial institutions, including J.P. Morgan, are already exploring blockchain solutions for internal operations and payments.

Q5: When will blockchain be mainstream?

Blockchain adoption is already happening in several industries. Current applications include cross-border payments, supply chain tracking, digital identity verification, and automated agreements. By 2030, blockchain could become an invisible foundation behind many digital services.

You may not directly “use blockchain” in the future — instead, you will use applications built on blockchain technology without realizing it, just like you use the internet without thinking about the protocols and servers that power it.